Summary

- The federal debt is $28.3 trillion and rising.

- The trade deficit is worsening.

- Inflation has arrived.

- The US dollar is depreciating.

This article considers the present plight of the US dollar with respect to the federal debt, the trade deficit, inflation and depreciation. Investors should pay attention to the development of these factors and make timely investment decisions in order to preserve their wealth.

Federal Debt

More and more investors are paying attention to the size of the federal debt. It is $28.34 trillion, which is 127% of GDP. See the debt clock (U.S. National Debt Clock: Real Time). In 2020 the ratio of Italy’s debt to GDP was 155%. In 2020 Greece reached an ATH (All Time High) of debt to GDP of 205%. The Biden administration has proposed a federal budget of over $ 6 trillion for the coming fiscal year and deficits for the next 6 years. One could ask the question if the US is going to be in the same class as Greece and Italy. Even considering such a possibility is alarming and drastic. Such prospects do not seem to have deterred the current administration from making even more debt. It is reasonable to assume that faith in US paper (Treasuries) and the US dollar is going to diminish as the federal debt continues to grow.

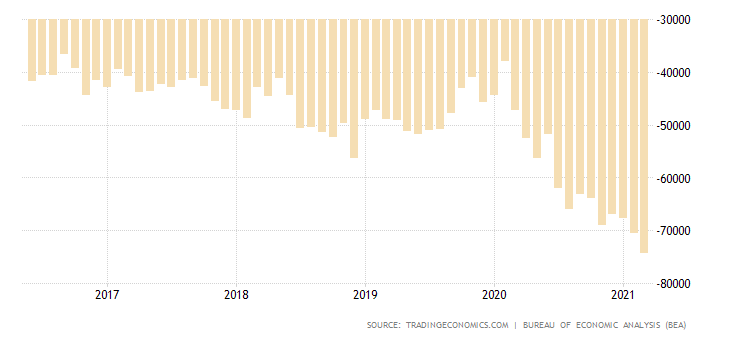

Trade Deficit

The trade deficit is not improving. The 5-year chart below shows the effects of the pandemic in 2020 and the effects of increased demand later the same year and in 2021.

The current trade deficit is at record highs, and this has not gone unnoticed by the MSM (Main Stream Media):

US trade deficit hits record $74.4 billion in March

The trade deficit should logically lead to a weaker US dollar.

Inflation

So much has been written about inflation recently that one wonders why it took so long for commentators to notice it. The answer to that question is that the extent of the growth in inflation is extremely difficult to overlook. It should be no surprise that the extensive growth in the money supply engineered by the Fed has contributed to rapid price increases. The Fed’s insistence that inflation is temporary does not mean that inflation is going to go away anytime soon. The government stimulus plans have put a lot of money in the pockets of consumers. Pent-up demand resulting from pandemic lockdowns means that a lot of money is chasing a smaller amount of goods and services. Inflation is the result.

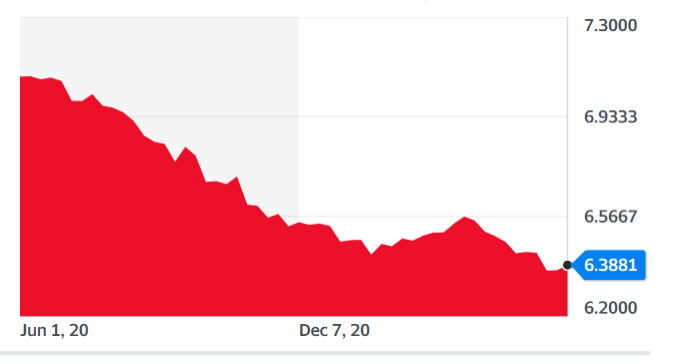

US Dollar Depreciation

One can only expect that higher inflation rates will not be conducive to supporting the value of the US dollar in Forex markets. The dollar has been weaker over the last year.

DXY | U.S. Dollar Index (DXY) Advanced Charts | MarketWatch

The trend is definitely lower, and there is no need to belabor the point.

The Bottom Line

Investors should be aware of the increase in federal debt, the record trade deficit, the growth of inflation and the depreciation of the US dollar. This writer has continually suggested that diversification away from the US dollar is one way that investors can protect their wealth. The US dollar is still a strong currency even if the dollar index is now below 90. Gold is of course a good hedge against inflation, and real estate is something solid and tangible that usually keeps its value although not always. In addition to these traditional investments, given the present situation, diversifying away from the US dollar is another possible strategy for investors. This does not mean that one should sell all of one’s dollar holdings. The depreciation of the dollar will probably be gradual due to the fact that two-thirds of global debt is dollar denominated. The demand for dollars is not going to collapse. However, assuming that dollar depreciation is going to be gradual, it is reasonable to start diversification as soon as possible because the dollar is still trading at a high level in Forex markets.

Another reason for diversification now is that the present geopolitical situation is extremely tense, and sudden events cannot be excluded. In addition, the PBoC is promoting its CBDC (Central Bank Digital Currency), and the renminbi is strengthening against the US dollar. In other words, the US dollar buys fewer yuan.

Source: BLS

Dollar depreciation may accelerate after the new Basel III rules take effect. This will probably bring about an increase in the price of gold as it will no longer be so easy to manipulate the gold bullion market. There is great demand for physical gold, and this will push up the price, which is quoted in US dollars. This will be evident on a global scale and will help to reinforce the impression that the US dollar is suffering from inflation.

Lastly one can add that the dollar is overvalued. That is another topic that should be treated in a separate article. In any case hopefully it has been made clear to investors that a dollar storm is brewing. It is better to batten the hatches in good time before the weather worsens. There is still time to make good investment decisions. Better sooner than later.

Seeking Alpha

Jun. 03, 2021 1:00 AM ETUUPUDNUSDU1 Comment

https://seekingalpha.com/article/4432774-debt-dollar-depreciation#comments

This article was written by

![]()

Long-Term Horizon, Contrarian

Contributor Since 2018

B.A., M.A., University of Pennsylvania,; M.A., (Oxon.); Ph.D. Princeton University Currently CEO of WWS Swiss Financial Consulting SA

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Data from third-party sources may have been used in the preparation of this material and WWS Swiss Financial Consulting SA (WWW SFC SA) has not independently verified, validated or audited such data. WWS SFC SA accepts no liability whatsoever for any loss arising from use of this information, and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Please consult your own professional adviser before taking investment decisions.

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

All investments involve risk, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Data from third-party sources may have been used in the preparation of this material and WWS Swiss Financial Consulting SA (WWW SFC SA) has not independently verified, validated or audited such data. WWS SFC SA accepts no liability whatsoever for any loss arising from use of this information, and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Please consult your own professional adviser before taking investment decisions.

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

All investments involve risk, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments.